Innovation isn’t new.

We’ve been planning, developing, launching, and improving new products, services, and businesses since the dawn of mankind. From Stone Age tools to the AI tech that will power our future robot masters*, innovation has been the driving force behind our progress as a species.

* Don’t let those "Robot Fights Back” videos fool you: first, they’re fake; second, science says AI uprisings are highly unlikely.

Innovation is a pillar of business growth

In any context, innovation is more than simply developing or implementing a new tool or process. The fundamental goal of innovation is the creation of “options for future growth”[1]. Stone Age tools advanced our ancestors’ abilities to build, hunt, and create. The benefits of today’s machine learning business applications include increased efficiency, greater cost savings, and better customer experiences — all of which help businesses grow.

It’s important to note that innovation doesn’t mean a unique product or service. Just look at Google — when it comes to, say, search engines, email clients, and browsers, we were content to use other highly capable services. Google didn’t reinvent the virtual wheel; they innovated online experiences, and then brought the same logic to hardware products like smartphones, laptops, and smart home devices.

Silicon Valley giants, and the startups clawing at their heels, foster cultures of innovation. As Steve Jobs said, “innovation is the ability to see change as an opportunity, not a threat."[2]

Why corporate innovation fails

Since innovation comes in many forms, so too does innovation failure. Sometimes it arises from external factors like bad timing or changing consumer trends. More often, the key source of failure comes from within an organization itself.

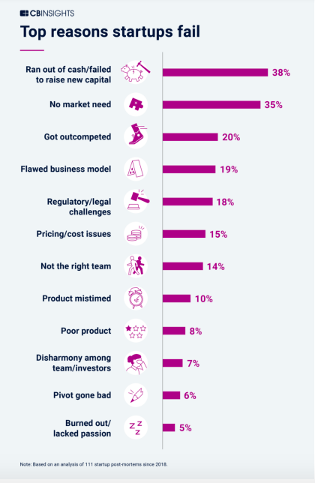

In 2021, market research firm CB Insights analyzed 111 failed startups across the world to find the most common reasons for their lack of success[3]. Since startups are, almost by definition, hubs of ideation and innovation, the resulting report helps frame how to think productively about innovation failure in general. The top three reasons (out of a total of 12) the surveyed businesses sank were:

Insufficient capital (38%)

Lack of market need (35%)

Inability to keep up with the competition (20%)

Flawed business models, regulatory issues, mistimed product launches, and disharmony among stakeholders also featured prominently on the list.

Source: https://www.cbinsights.com/reports/CB-Insights_Top-Reasons-Startups-Fail.pdf

At first glance, these causes of failure may seem too disparate to draw useful lessons from. In fact, there are a few common threads running through them, in particular inadequate resources and unclear go-to-market strategies.

Innovation is about more than just creating ideas. It’s an end-to-end process that runs from ideation to execution, encompassing a variety of practical activities. Smart resource allocation, therefore, is crucial if you are going to turn an idea into something commercially viable.

Poor or non-existent strategy also accounts for a large percentage of startup failures, as the above findings indicate. The success or failure of an innovation is closely related to the processes used by the organization behind it. In the words of tech entrepreneur and U+ Managing Partner Sean Sheppard: “External market forces matter, but having the right mindset, skillset, experience level, and go-to-market framework is what really makes the difference in deciding which innovations succeed.”

How to drive innovation to success

1. Know your value proposition and product-market fit

A value proposition is a statement that identifies the benefits your customer gets from buying your product. By articulating these benefits in a clear and measurable way, you can laser-focus on where your innovation’s value lies from day one — and avoid getting caught up in the inessential details. A good value proposition may take any number of forms, but it will always answer the following questions:

Who are my potential customers?

Where can I find them?

What specific problem does my innovation solve?

Is the market big enough to justify the project?

Once you have a strong understanding of your market, you can begin to establish your product-market fit. In the words of venture capitalist Marc Andreessen, who coined the term in an influential blog post[1], product-market fit simply means “being in a good market with a product that can satisfy that market.”

The search for product-market fit leaves little room for sentimentality: it requires an experimental mindset and a readiness to pivot if needed. At this stage of your product’s lifecycle, you should treat every interaction you have with a potential customer as data to be parsed. All this data should be directed towards solving the problem you’ve identified in the research phase.

After you have market-verified your value proposition, the next step in your innovation journey will be to rigorously define the product. Bear this chronology in mind: the second most common cause of startup failure according to the CB Insights report cited above was a lack of market need.

“Lack of differentiation is a major pitfall for corporate innovators,” says Sean Sheppard. “That’s why you need to know your market just as fully as you know your product.”

2. Define your product

During the product definition stage, your innovation should begin looking more and more like a commercially-viable product. This is when you cast aside all the vague potential things your idea could be and ruthlessly identify the one thing it has to be.

Create an identity. This means choosing names, logos, color schemes, and early advertising content.

Explore marketing strategies. You already know how brilliant and useful your innovation is. Now it’s time to tell your customers too.

Build your team. Early employees have a profound effect on a company’s identity and culture, and on whether it floats or sinks. Your initial team should have as strong a grasp of your product’s potential, and be as excited about it, as you.

Understand pricing. As your innovation moves from idea to product, you can now consider the best pricing strategy. Whether you choose a subscription or one-off payment model, a budget or a premium price, will depend entirely on the market your product is serving.

3. Launch your minimum viable product

Your minimum viable product, or MVP, is the earliest version of your product that customers can actually use to solve their problem. As you progress towards the launch date, you should choose the technology that underpins your MVP. You’lll need the right programming language, development tools, and infrastructure. You may want a cloud or dedicated server, depending on your needs (more on that here). Of course, you’ll also need the right team, including platform-specific developers with enough experience. If this is too much of a challenge, then it might be time to work with an external agency as you build out the tech.

Next, you must calculate your customer lifetime value (CLV) — i.e. the value of a given customer over the duration of their relationship with your business. This will likely take an improvised, back-of-the-napkin form at first. Once real customer data starts coming in, you can adjust your expectations accordingly. Above all, you must ensure that your CLV is higher than the costs associated with acquiring customers in the first place. Serial entrepreneur David Skok identifies high customer acquisition costs as the second biggest “startup killer” after poor product-market fit.[2] According to Skok, enthusiastic innovators often “grossly underestimate the cost it will take to acquire customers” and end up paying for it with the future of their business. Avoid this trap.

4. Don’t stop iterating

With an early version of your product now on the market, you can now move to the “final” stage in the innovation process: iteration. This stage typically involves making product modifications based on early customer feedback. It’s also when you can start thinking seriously about the costs and logistics of scale. As always, the conclusions you come to should be grounded in genuine data, not unsupported assumptions. The more data you acquire, the smarter your process will be as you turn your MVP into a fully-fledged consumer product.

[1] Kupp & Kromer, Kromatic, Innovation Portfolio Management

[2] Carmine Gallo, Forbes, The 7 Innovation Secrets of Steve Jobs

[3] CB Insights, The Top 12 Reasons Startups Fail (Analysis of 111 global startups registered on the CB Insights database that failed since 2018)

[4] Marc Andreessen, Pmarca, Guide to Startups Part 4

[5] David Skok, For Entrepreneurs, Startup Killer: The Cost of Customer Acquisition

[1] Marc Andreessen, Pmarca, Guide to Startups Part 4

[2] David Skok, For Entrepreneurs, Startup Killer: The Cost of Customer Acquisition

Jan Beránek

Group CEO at U+Jan Beránek is chief executive officer and founder for U+, a leading global digital product development company, specializing in corporate research and development, the launch of corporate and startup innovations, and the transformation of Fortune 1000 companies’ digital ideas into real products. During the past 12 years, U+ has successfully turned more than 90 ideas into reality with total valuation exceeding $1B in the fintech, energy, telco, e-health and automotive industries. For more information, please visit https://u.plus/.