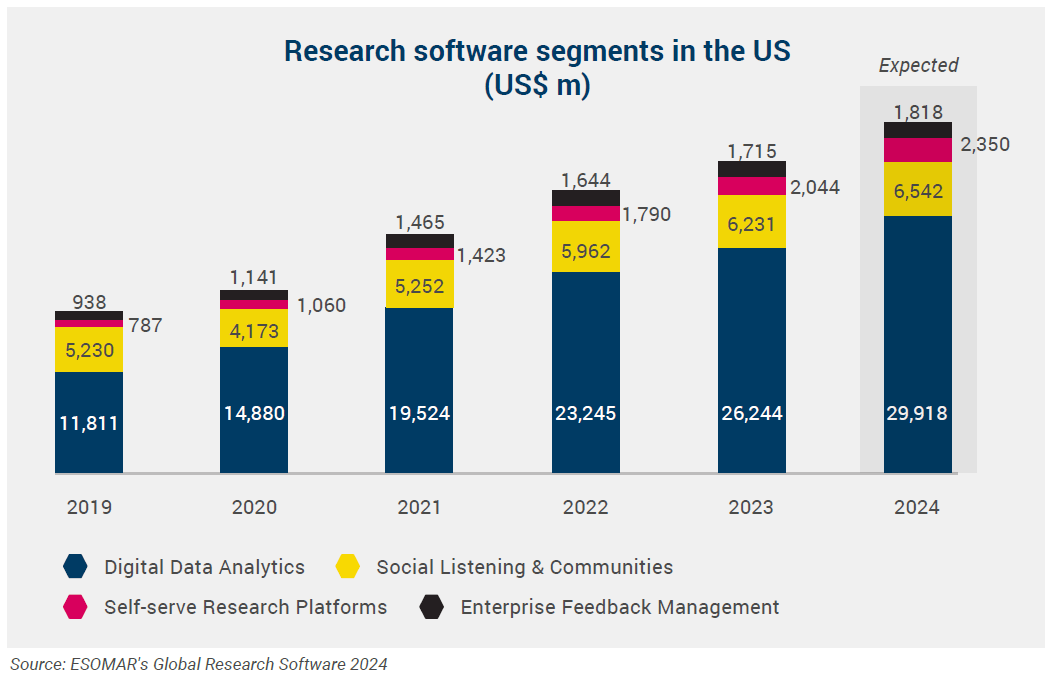

The US research software market experienced notable growth between 2019 and 2023, mainly driven by digital data analytics. This segment grew by 12.9% between 2022 and 2023, reaching US$26.2 billion in 2023, compared to US$11.8 billion in 2019. Representing 72% of the total US market in 2023, digital data analytics’ dominance highlights the industry’s focus on leveraging advanced data tools for strategic decisions. This reliance on data-driven insights will likely continue, with organisations seeking more sophisticated analytics capabilities.

While growing at 4.5% in the last year, social listening and communities captured 17% of the market, reflecting its steady role in consumer sentiment analysis. As social media continues to influence businesses, this segment’s relevance is expected to grow, although not as rapidly as other sectors.

The most exciting development is the 14% growth in self-serve research platforms. Alternatively known as DIY platforms, this segment represents almost 6% of the sector’s turnover in the US, indicating the shift toward democratising these research tools. A possible implication is that more organisations, even small-scale firms, are adopting these flexible, cost-effective platforms to extract insights rather than relying on conventional full-service agencies. For the industry, this trend means increased competition for full-service market research firms and opportunities for hybrid models that combine professional research guidance with self-service technology.

Enterprise feedback management (EFM) grew by 4.3%, showing stable but moderate demand as companies focus on improving customer experience through feedback systems.